Healthcare in America Overview

It’s difficult to keep up with all the chaos these days. That’s why I started Trillions National Weekly. Just read or listen to Trillions once each week. We keep you up-to-date on national news with nonpartisan commentary in a concise 15-minute read (or listen to the newsletter on the Substack app).

Take a few weeks to familiarize yourself with the newsletter—and the extensive resources on this website—then beginning March 1, 2026, the resources and newsletter will be available to all paid subscribers for only $5/month or $50/year.

If you subscribe by February 28th, you’ll receive a 20% discount—$4/month or $40/year.

All of this up-to-date, nonpartisan content is easily accessible by typing TrillionsWeekly.com into your browser.

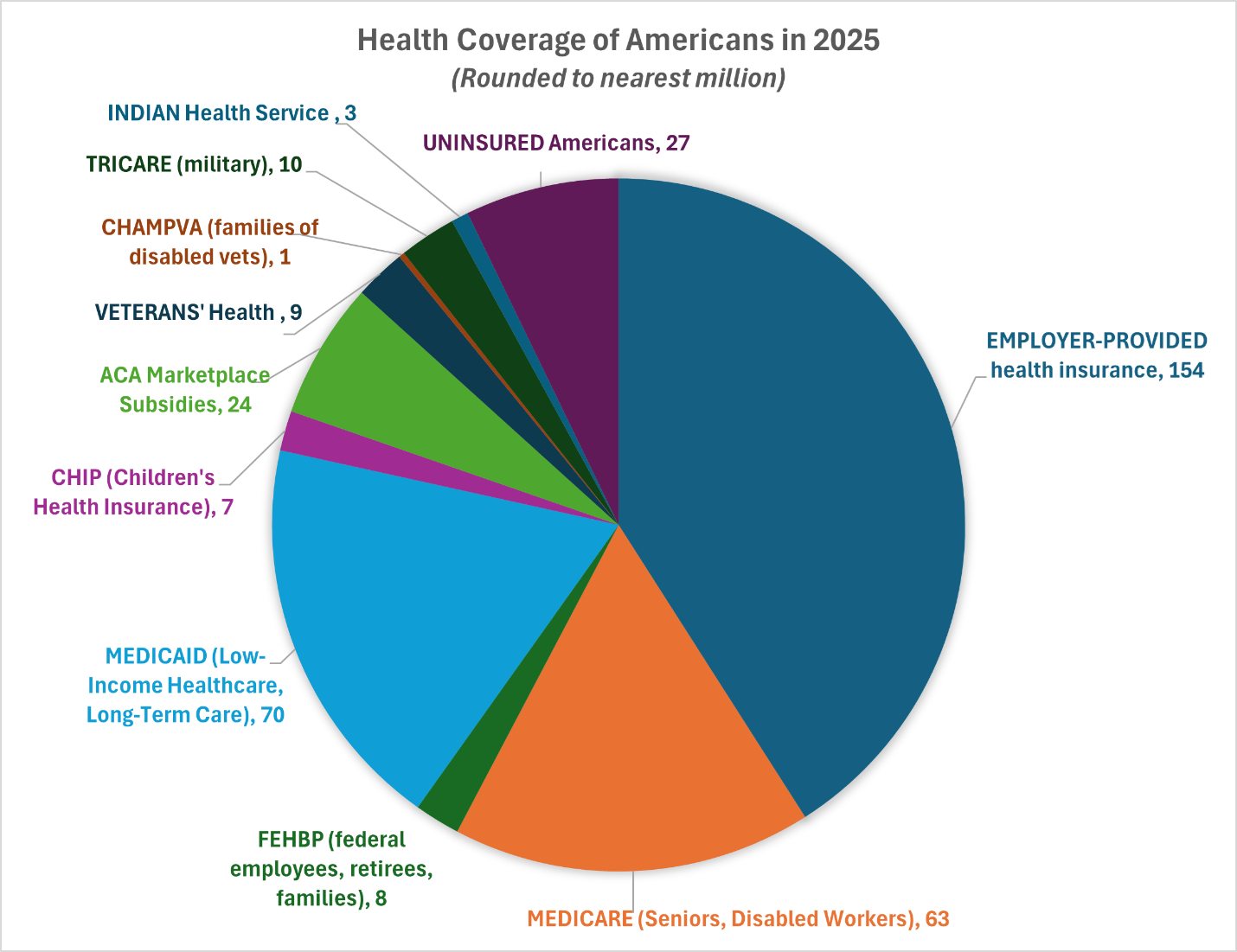

Important note: Medicaid and Medicare are often confused but are entirely different programs serving different populations. Medicaid is a joint federal-state program that pays healthcare and long-term care providers for care provided to low-income Americans, while Medicare is a federal health insurance program covering all people 65 and older and disabled workers and disabled adult children of retirees. Some low-income seniors and disabled Americans are covered by both programs.

America has a patchwork quilt of healthcare coverage which depends on age, income, employment status, civilian or military service, and health status:

Employer-provided health insurance plans cover about 3 out of 5 Americans under age 65.

Medicare is a national health insurance system, covering nearly 70 million—roughly 1 in 5—Americans. Medicare covers Americans who are ages 65 and older, disabled workers, disabled adult children of retirees, and people with end-stage renal disease or ALS (due to the extraordinary healthcare costs). Medicare is financed by federal payroll taxes, general revenues, and premium payments. Traditional Medicare, as an insurance system, pays participating healthcare providers fees for specific services. The newer Medicare Advantage program, makes per person annual payments to private sector Medicare Advantage plans.

Medicaid is the nation’s largest single source of health coverage. It covers more than 70 million—roughly 1 in 5—Americans. Medicaid pays for healthcare for people at or below the federal poverty level (and, in some States, people marginally above the poverty level). The program is financed jointly by the federal and state governments, but is administered by the States. State Medicaid plans pay healthcare providers in one of two ways: payments to providers for specific services, or monthly per person payments to approved managed care plans. States also make payments to hospitals and clinics that serve large Medicaid populations.

The Children’s Health Insurance Program (CHIP) provides low-cost health coverage to children in low-income families that earn too much money to qualify for Medicaid but not enough to purchase insurance on their own. It covers more than 7 million children.

Veterans’ Health Administration hospitals and facilities provide direct healthcare to about 9 million veterans with service-connected disabilities and/or low incomes. The system operates over 170 medical centers and nearly 1,200 outpatient clinics, serving millions of veterans across the nation.

TRICARE is the uniformed services health care program for active duty service members and their families, National Guard and Reserve members and their families, retirees and family members, and survivors. It covers nearly 10 million Americans.

CHAMPVA (Civilian Health and Medical Program of the Department of Veterans Affairs) is a health insurance program for dependents and survivors of a veteran who was permanently and totally disabled by a service-connected disability. It covers about 730,000 Americans.

FEHB (Federal Employee Health Benefits Program) covers current federal employees, federal retirees, and their families—about 8 million Americans (2.4% of the population).

Indian Health Service facilities provide direct healthcare to nearly three million American Indians and Alaska Natives across 37 states.

The Affordable Care Act was enacted in March 2010 to close a large gap in U.S. healthcare, with millions of Americans lacking access to affordable health insurance. The ACA expanded access by: (1) enabling states to expand Medicaid coverage (with 90 percent federal funding) to people earning slightly above the federal poverty level; and (2) providing subsidies to purchase private health insurance for people with low and middle incomes who are not eligible for Medicare, Medicaid, or CHIP (Children’s Health Insurance). In 2025, more than 46 million people have coverage through ACA subsidies or Medicaid expansion. Key facts about the ACA:

The ACA subsidies, delivered as tax credits, are used to purchase private insurance through online health insurance “exchanges” established by the states, or through the federal exchange in states that have not established their own. In 2025, the income eligibility cap for subsidies is $60,600 for individuals and $128,600 for a family of four. In 2021, the American Rescue Plan Act (ARPA) expanded eligibility for, and increased, ACA health insurance subsidies, which were extended through 2025 by the Inflation Reduction Act (IRA). The enhanced subsidies have now expired.

Strong public support: In 2025, 64 percent of U.S. adults hold a favorable view of the ACA.

ACA Protects people with pre-existing conditions: The ACA prohibits insurance companies from denying coverage or charging higher premiums due to pre-existing conditions—one of the key reasons that people lacked coverage prior to the ACA.

ACA Prohibits Lifetime Limits on Benefits: The ACA prohibits insurance plans from capping lifetime coverage of essential benefits to protect people with chronic and acute health conditions.

ACA Capped out-of-pocket costs: All policies must provide an annual maximum out-of-pocket payment cap. After the cap is reached, all remaining costs are paid by the insurer.

ACA requires that plans not charge for preventive care, vaccinations, and medical screenings such as mammograms and colonoscopies.

ACA provided incentives for small employers to provide health insurance with tax credits up to 50% of their employer’s contribution.

ACA expanded coverage to young people by allowing adult children to remain on their parents’ plans until age 26.

Uninsured – 27 million: About 27 million (8% of the U.S. population) do not have any form of health insurance or coverage. The rate is comparatively higher in states that did not expand Medicaid under the Affordable Care Act.